Secure 2.0 was an extensive 2022 expansion of the original 2019 Secure Act. Hidden away in its 90+ provisions that impact 401(k), 403(b), and other qualified plans are changes that can be a catalyst for helping employees improve their retirement planning efforts. Secure 2.0 is all about making saving for retirement easier and more accessible – opening up company 401(k) plans to more employees. But it’s done more than just make changes to the plans themselves – it’s also reshaping retirement planning.

Workers today are struggling to save toward a financially secure retirement after their working days are over. Uncertainty about the economy, housing prices, interest rates, and even the price of basic food items are eating away at their confidence to afford stepping away from their jobs. Many are even considering working into their 70s.

The savings gap – Secure 2.0 to the rescue!

The Savings Gap

This all goes to show on a practical level what the experts have been talking about for some time – there’s a real retirement savings gap in America. It’s the difference between what employees have saved for retirement and the actual amount they’ll need to live comfortably once they get there.

Part of the reason is that too many employees don’t start saving early enough. The reasons vary – student loans to repay, buying a first home, or setting aside money for a dream vacation. But waiting to start saving, even for a few years, can be costly – both in how much an employee needs to save every year to try and catch up and in the amount they’ll ultimately have at retirement.

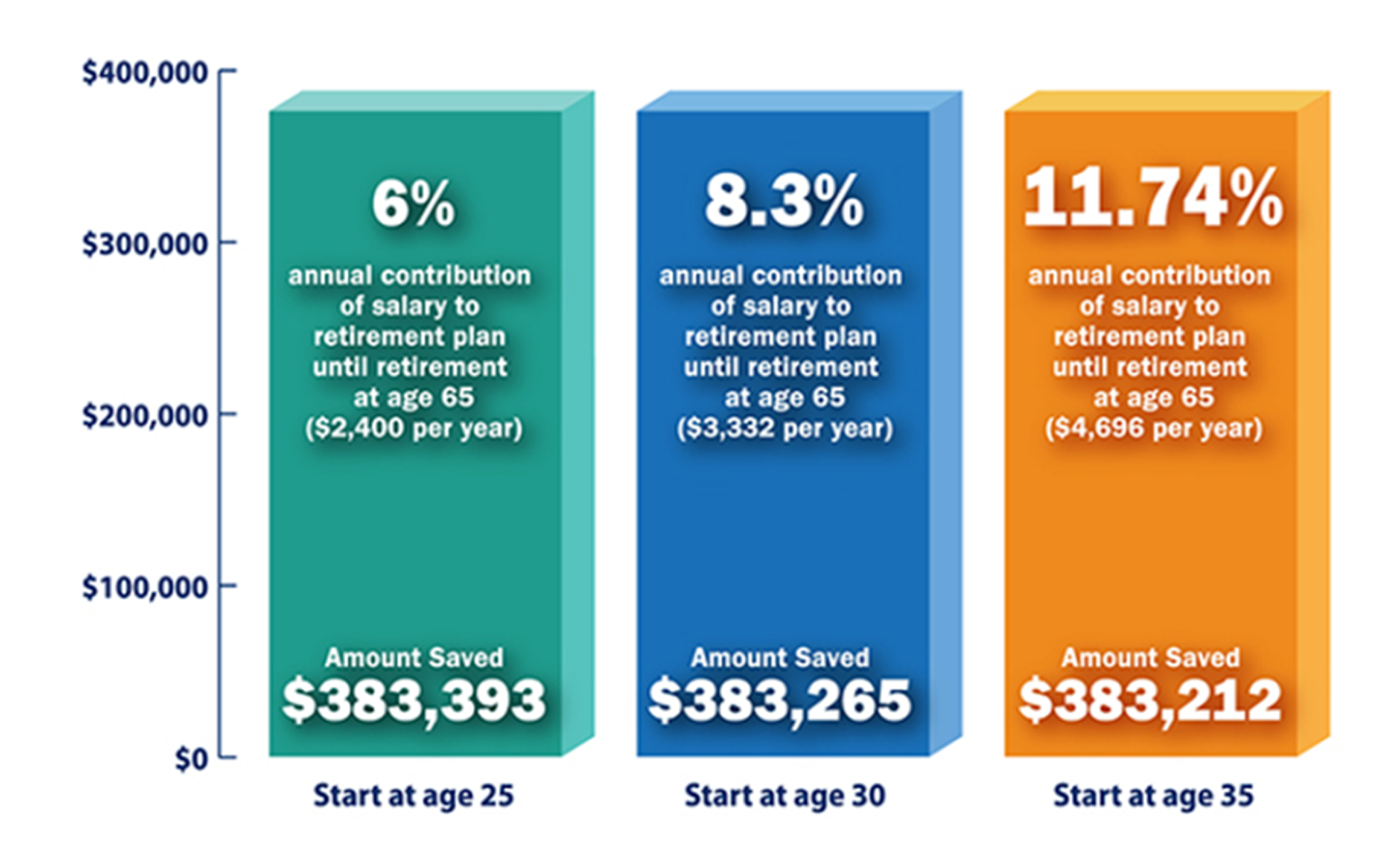

The following chart from the Mutual of America Financial Group shows how waiting affects a savings balance – in this case, a target of almost $400,000 at age 65.

Waiting just 10 years to start saving means having to save twice the amount each year to end up with about the same amount at age 65.

And even then... $380,000 probably isn’t nearly enough to fund a comfortable retirement. How much is? Most people have no idea how much they’ll need.

Financial experts estimate that to have $40,000 a year in retirement income, a person would need to have saved about $1 million – assuming a 4% annual withdrawal rate. That puts a sharp focus on the importance of saving more and starting sooner.

Retire in comfort? Secure 2.0 makes saving more easier.

There’s yet another problem. What about those employees who aren’t participating in their 401(k) plan? That often means no retirement savings at all. According to reports, nearly half of U.S. employees don’t have access to a 401(k) plan – many small businesses don’t even offer one. The result? In 2024, 1 in 5 Americans age 50+ found themselves with no retirement savings, according to an AARP survey.

Secure 2.0 To The Rescue!

Enter Secure 2.0. It’s a transformative piece of legislation aimed at boosting retirement savings and streamlining the paths employees can take toward greater financial security. It includes provisions to help employees save more, save earlier, and reach those who aren’t participating at all. It also helps employers implement the changes – some of which are mandatory, while others are optional.

Automatic Enrollment Changes: Automatic savings can give a big boost to an employee’s retirement security while increasing employee participation and savings in the company’s 401(k) plan. Beginning January 1, 2025, Secure 2.0 expands auto-enrollment and auto-escalation to all new 401(k) plans. Instead of waiting for employees to voluntarily opt in, new plans will now enroll them automatically, when they’re eligible, starting with at least 3% of their pay.

What it means: It provides a crucial nudge for those who tend to procrastinate about saving for retirement.

Higher 401(k) Catch-up Contributions: Catch-up contributions aren’t new – they’ve been around since 2001, allowing older workers to stash more money away by contributing extra amounts above the regular limits beginning at age 50. Secure 2.0 enhances that provision by allowing higher contributions of up to $11,250 (indexed for inflation) for employees aged 60–63, starting in 2025.

What it means: This feature is especially helpful for those who didn’t start saving early or who’ve fallen behind and want to catch up.

Inclusion of Full-Time Part-Time Employees: Secure 2.0 expands access to tax-qualified savings for long-term part-time employees by allowing them to participate in their company’s 401(k) plan once they’ve worked at least 500 hours/year for two consecutive years. They may not be eligible for matching contributions, but it’s still a valuable way to start building a retirement nest egg.

What it means: It’s a way to bring more employees into the savings conversation. Part-time workers now have a way to save for retirement with tax-deferred money.

Delayed RMDs: Required Minimum Distribution (RMD) rules dictate when retirees must begin taking money from their 401(k) retirement accounts, with amounts withdrawn based on the retiree’s age and account balance. Secure 2.0 pushes the RMD starting age to 73 for those born between 1951 and 1959.

What it means: Delaying withdrawals allows more time for retirement accounts to grow before distributions begin.

Student Loan Assistance: Paying off student loans while trying to save for retirement can feel impossible. Secure 2.0 allows employers to match an employee’s student loan repayments with contributions to their 401(k) – treating their loan payments as if they were salary deferrals.

What it means: This provision can help younger employees start building retirement savings even if they have other financial obligations and can’t afford to make contributions at that time.

Secure 2.0 has new payment options – check ‘em out here!

Emergency Savings Accounts: Secure 2.0 introduces an emergency savings account option within 401(k) plans, allowing employees to set aside up to $2,500 in it with penalty-free access and the possibility of employer matching contributions. Adoption, however, has been slow due to administrative complexities.

What it means: Encourages saving for financial emergencies while also providing an easy way for employees to access emergency funds without dipping into their long-term 401(k) savings.

Lifetime Income Options and Annuities: Annuities can provide retirees with a steady income stream. Secure 2.0 provisions make it easier to include annuities in 401(k) plans, allow employees to move annuities between plans without penalties, and require 401(k) statements to include annuity illustrations.

What it means: Annuities are more attractive and understandable for employees and employers alike.

Staying on Track to Reshape Retirement Savings

Secure 2.0 is reshaping retirement planning by expanding opportunities for employees to save for retirement and enhancing employer-sponsored 401(k) plans. It’s more than just features – it’s about helping employees understand why saving early matters, how much they may need, and how their 401(k) plan can help them get there.

Employers have an important role to play in these changes – they can make saving for retirement more accessible, less stressful, and easier to follow through with. By helping plan sponsors communicate these changes clearly and effectively, TPAs can play a central role in shaping better outcomes – for sponsors and employees alike.

Let Stax.ai Help You Stay on Track

At Stax.ai, we help TPAs support plan sponsors with accurate, accessible, and automated plan data that eliminates manual tasks. Our revolutionary AI-driven solutions simplify administration and make it easier to stay compliant so you can help sponsors focus on what really matters: helping employees retire with confidence.

Want to know how? Contact us for more information or to request a demo.

Next

Why TPA Cybersecurity Builds Client Trust

Census Data Scrubbing – What a Chore!

Automate your Census Workflow.

Simplify annual census collection through effortless payroll data gathering and automated scrubbing based on plan document provisions.

Simplify annual census collection through effortless payroll data gathering and automated scrubbing based on plan document provisions.